Which of the following is the least useful method or model to calculate the value of a real option in a project?

The following cash flows are expected:

- 10 yearly payments of $80, with the first payment in 6.5 years from now (first payment at t=6.5).

- A single payment of $500 in 4 years and 3 months (t=4.25) from now.

What is the NPV of the cash flows if the discount rate is 10% given as an effective annual rate?

Question 639 option, option payoff at maturity, no explanation

Which of the below formulas gives the payoff ##(f)## at maturity ##(T)## from being short a put option? Let the underlying asset price at maturity be ##S_T## and the exercise price be ##X_T##.

Question 852 gross domestic product, inflation, employment, no explanation

When the economy is booming (in an upswing), you tend to see:

Question 884 monetary policy, impossible trinity, foreign exchange rate, no explanation

According to the impossible trinity, a currency can only have two of these three desirable traits: be fixed against the USD; convertible to and from USD for traders and investors so there are open goods, services and capital markets; and allow independent monetary policy set by the country’s central bank, independent of the US central bank.

Which of the following exchange rate regimes sacrifices fixing the exchange rate to the USD? In other words, which regime uses a floating exchange rate?

Question 903 option, Black-Scholes-Merton option pricing, option on stock index

A six month European-style call option on the S&P500 stock index has a strike price of 2800 points.

The underlying S&P500 stock index currently trades at 2700 points, has a continuously compounded dividend yield of 2% pa and a standard deviation of continuously compounded returns of 25% pa.

The risk-free interest rate is 5% pa continuously compounded.

Use the Black-Scholes-Merton formula to calculate the option price. The call option price now is:

A non-dividend paying stock has a current price of $20.

The risk free rate is 5% pa given as a continuously compounded rate.

Options on the stock are currently priced at $5 for calls and $5.55 for puts where both options have a 2 year maturity and an exercise price of $24.

You suspect that the call option contract is mis-priced and would like to conduct a risk-free arbitrage that requires zero capital. Which of the following steps about arbitraging the situation is NOT correct?

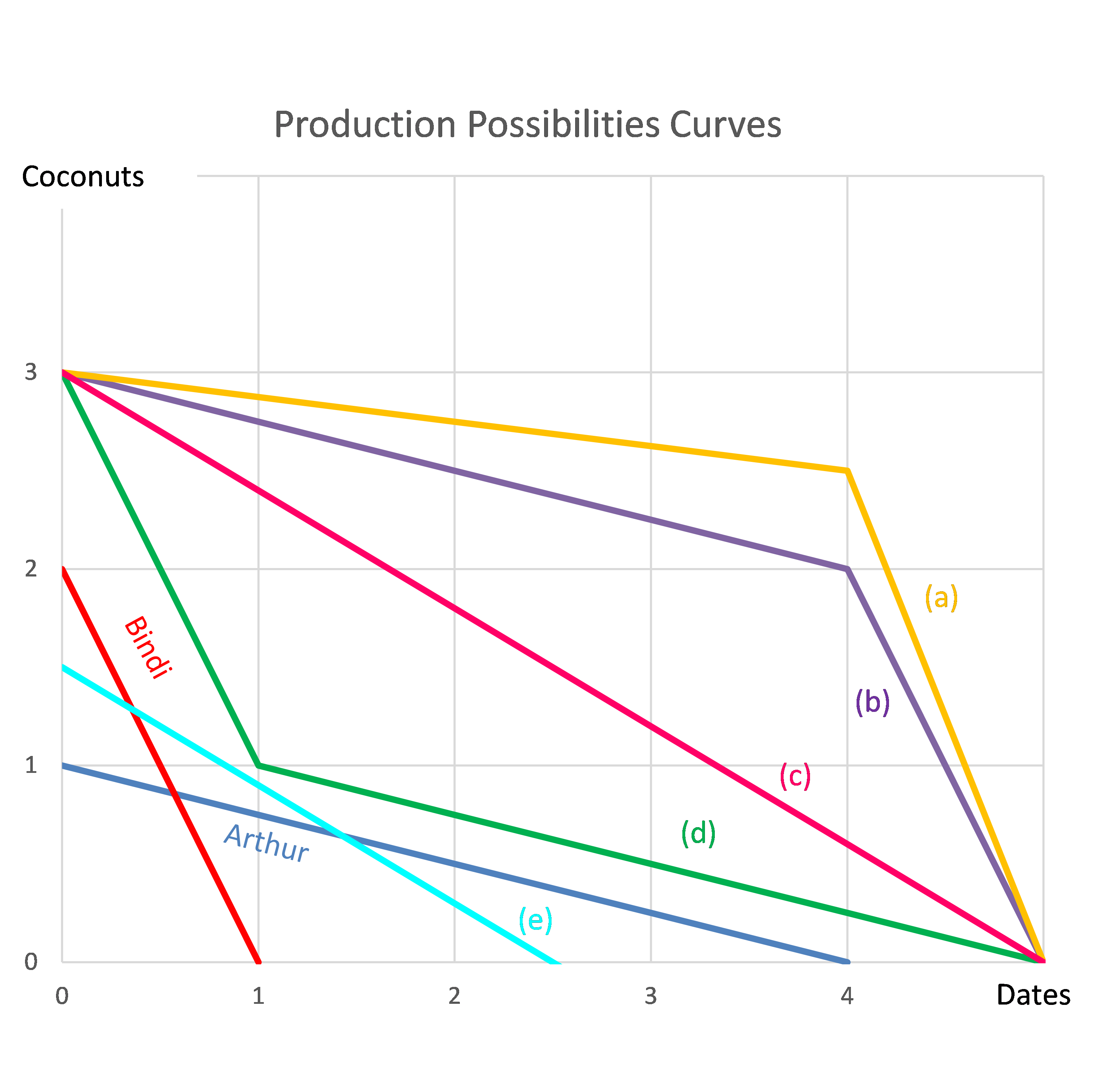

Question 978 comparative advantage in trade, production possibilities curve, no explanation

Arthur and Bindi are the only people on a remote island. Their production possibility curves are shown in the graph.

Assuming that Arthur and Bindi cooperate according to the principles of comparative advantage, what will be their combined production possibilities curve?