The saying "buy low, sell high" suggests that investors should make a:

If an investor buys at a low price and then sells at a higher price, then she has made a positive capital return. This is the answer to the question.

The equation that breaks total returns into income and capital returns is:

###\begin{aligned} r_\text{total}&=r_\text{income}+r_\text{capital} \\ &=\dfrac{C_1}{P_0} +\dfrac{P_1-P_0}{P_0} \\ \end{aligned}###The capital return is the last term:

###\begin{aligned} r_\text{capital} &= \dfrac{P_1-P_0}{P_0} = \dfrac{P_1}{P_0} - 1\\ \end{aligned}###The capital return will be positive when the sale price in one year ##(P_1)## is higher than the buy price now ##(P_0)##.

Commentary

The saying 'buy low, sell high' implies that capital returns are the best way to make money. While positive capital returns are certainly desirable, positive income returns are equally valuable, disregarding tax differences. Income cash flows ##(C_1)## occur in the form of dividends from stocks, rent from land or interest from debt.

The most important performance metric is the total return which is the sum of the capital and income returns. Investors seek high total returns on their wealth.

Given a constant total return, higher income returns actually reduce capital returns and vice versa. This can be seen when share prices fall following the payment of a dividend.

Total cash flows can be broken into income and capital cash flows. What is the name given to the income cash flow from owning shares?

Shares pay dividends. Note that paying a dividend is a form of 'equity payout' from the dividend-paying firm's perspective. From the shareholder's perspective the dividend is income.

An asset's total expected return over the next year is given by:

###r_\text{total} = \dfrac{c_1+p_1-p_0}{p_0} ###

Where ##p_0## is the current price, ##c_1## is the expected income in one year and ##p_1## is the expected price in one year. The total return can be split into the income return and the capital return.

Which of the following is the expected capital return?

The expected capital return is shown in answer d: ##r_\text{capital} = \dfrac{p_1}{p_0} - 1 = \dfrac{p_1-p_0}{p_0}##.

Answer a is the expected dollar income: ##c_1##.

Answer b is the expected dollar capital gain rather than return: ##p_1 - p_0##.

Answer c is the expected income return: ##\dfrac{c_1}{p_0}##.

Answer e is sometimes called the expected gross capital return: ##\dfrac{p_1}{p_0}##. Note that the gross return minus one equals the net capital return. Capital return and net capital return are used interchangeably. So ##r_\text{capital} = r_\text{net capital} = r_\text{gross capital} - 1##.

A share was bought for $30 (at t=0) and paid its annual dividend of $6 one year later (at t=1).

Just after the dividend was paid, the share price fell to $27 (at t=1). What were the total, capital and income returns given as effective annual rates?

The choices are given in the same order:

##r_\text{total}## , ##r_\text{capital}## , ##r_\text{dividend}##.

###\begin{aligned} r_\text{total} =& r_\text{capital} + r_\text{income} \\ =& \frac{P_1 - P_0}{P_0} + \frac{C_1}{P_0} \\ =& \frac{27 - 30}{30} + \frac{6}{30} \\ =& \frac{-3}{30} + \frac{6}{30} \\ =& -0.1 + 0.2 \\ \end{aligned}### So the capital return was -0.1 and the income return was 0.2. The total return is the sum: ### r_\text{total} = 0.1###

One and a half years ago Frank bought a house for $600,000. Now it's worth only $500,000, based on recent similar sales in the area.

The expected total return on Frank's residential property is 7% pa.

He rents his house out for $1,600 per month, paid in advance. Every 12 months he plans to increase the rental payments.

The present value of 12 months of rental payments is $18,617.27.

The future value of 12 months of rental payments one year in the future is $19,920.48.

What is the expected annual rental yield of the property? Ignore the costs of renting such as maintenance, real estate agent fees and so on.

The rental yield, also called the income return, of a property is calculated as the dollar income at the end of the period divided by the current market price.

The future value of the annual rent cash flow ($19,920) is used as the income cash flow ##C_1## since the income return (##r_\text{income}##) is supposed to be the cash income received at the end of the year (t=1) divided by the market price now (t=0):

###r_\text{rent} = r_\text{income} = \dfrac{C_1}{P_0} = \dfrac{19,920}{500,000} = 0.039841###Notice that the current market price is $500,000, compared to the old market price of $600,000. The old price of $600,000 could be called the historical cost or book value. The current market price is the best estimate of how much the asset is actually worth if it was sold right now. That's why financiers prefer to always know the current market price. However, accountants prefer to use book prices because they're more certain, despite the fact that they are old, stale and a little useless.

Question 542 price gains and returns over time, IRR, NPV, income and capital returns, effective return

For an asset price to double every 10 years, what must be the expected future capital return, given as an effective annual rate?

There's no mention of income cash flows such as dividends or rent so we'll ignore them. The capital return ##(r_\text{cap})## leading to the price rise can be calculated using the 'present value of a single cash flow' formula.

###P_0 = \dfrac{P_{10}}{(1+r_\text{cap})^{10}} ###For the price to double in 10 years, then ##P_{10}## will be twice ##P_0##, so ##P_{10} = 2P_0##. Substitute this into the above equation and solve for the capital return.

###P_0 = \dfrac{2P_{0}}{(1+r_\text{cap})^{10}} ### ###\begin{aligned} (1+r_\text{cap})^{10} &= \dfrac{2P_{0}}{P_0} \\ &= 2 \\ \end{aligned}### ###{\left( (1+r_\text{cap})^{10} \right)}^{1/10} = {2}^{1/10}### ###1+r_\text{cap} = {2}^{1/10}### ###\begin{aligned} r_\text{cap} &= 2^{1/10} - 1 \\ &= 0.071773463 \\ \end{aligned}###Question 278 inflation, real and nominal returns and cash flows

Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year.

Inflation is the proportional increase in price levels. An inflation rate of 2% means that a product that costs $10 now will cost $10.20 (=10(1+0.02)1) in one year.

If you have $1,000 in the bank right now, you can buy 100 (=1,000/10) products.

The bank interest rate is 1% so $1,000 in the bank will grow to be $1,010 (=1,000(1+0.01)1) in one year. Product prices are $10.20 at this time, so we can only buy 99 (or 99.02 =1,010/10.20) products rather than 100 products before.

Economist's method

An economist would say that the higher inflation rate has eroded our buying power.

A short cut to doing the calculations above is to find the real return using the Fisher equation,

###\begin{aligned} 1+r_\text{real} &= \frac{1+r_\text{nominal}}{1+r_\text{inflation}} \\ &= \frac{1+0.01}{1+0.02} \\ \end{aligned}###

###\begin{aligned} r_\text{real} &= \frac{1+0.01}{1+0.02} -1 \\ &= 0.990196078 -1 \\ &= -0.009803922 = -0.9803922\% \\ \end{aligned}###

This says that our real return is negative, so our wealth buys 0.98% less after one year, so instead of buying 100 products we can only buy 99.02 (=100(1-0.0098)) products in one year.

Note that the exact Fisher equation can be approximated:

###\begin{aligned} r_\text{real} &\approx r_\text{nominal} - r_\text{inflation} \\ &= 0.01 -0.02 \\ &= -0.01 = -1\%\\ \end{aligned}###

Commentary

This question was used in the '2004 Health and Retirement Survey' of Americans over the age of 50. The survey results were as follows:

- 75.2% of respondents answered it correctly,

- 13.4% were incorrect,

- 9.9% answered "don't know" and

- 1.5% refused to answer.

This question tests knowledge of inflation and was used in the research paper 'Financial Literacy and Planning: Implications for Retirement Wellbeing' by Annamaria Lusardi and Olivia S. Mitchell in 2011.

Question 993 inflation, real and nominal returns and cash flows

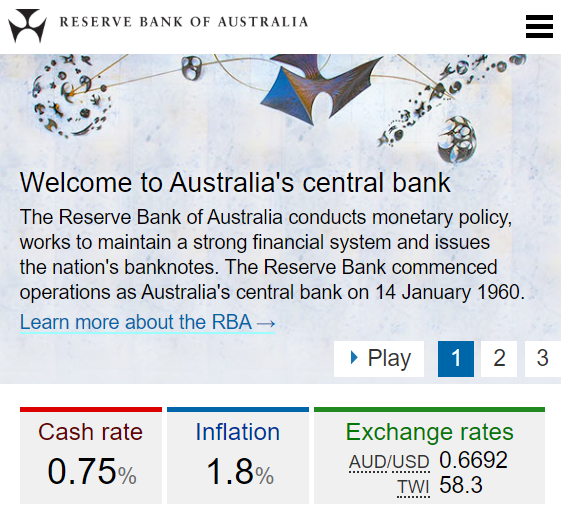

In February 2020, the RBA cash rate was 0.75% pa and the Australian CPI inflation rate was 1.8% pa.

You currently have $100 in the bank which pays a 0.75% pa interest rate.

Apples currently cost $1 each at the shop and inflation is 1.8% pa which is the expected growth rate in the apple price.

This information is summarised in the table below, with some parts missing that correspond to the answer options. All rates are given as effective annual rates. Note that when payments are not specified as real, as in this question, they're conventionally assumed to be nominal.

| Wealth in Dollars and Apples | ||||

| Time (year) | Bank account wealth ($) | Apple price ($) | Wealth in apples | |

| 0 | 100 | 1 | 100 | |

| 1 | 100.75 | 1.018 | (a) | |

| 2 | (b) | (c) | (d) | |

Which of the following statements is NOT correct? Your:

Real wealth at t=2 is $97.9477702 or 97.9477702 apples. To calculate this, we can find the real interest rate and grow current wealth by that real rate to find the real wealth at time 2.

The real interest rate is exactly equal to -1.0314342% pa using the Fisher formula:

###\begin{aligned} 1+r_\text{real} &= \dfrac{1+r_\text{nominal}}{1+r_\text{inflation}} \\ &= \dfrac{1+0.0075}{1+0.018} \\ \end{aligned}### ###r_\text{real} = -0.010314342###Real wealth at t=2 is then the current (t=0) wealth grown by the real interest rate over 2 years:

###\begin{aligned} \text{RealWealth}_2 &= \text{Wealth}_0(1+r_\text{real})^2 \\ &= \text{100}(1+-0.010314342)^2 \\ &= 97.9477702 \text{ apples or dollars}\\ \end{aligned}###Alternatively, real wealth at t=2 can be found by finding how many apples you can buy at this time, so divide nominal wealth by the nominal price of apples at time 2:

###\begin{aligned} \text{RealWealth}_2 &= \dfrac{\text{NominalWealth}_2}{\text{ApplePrice}_2} \\ &= \dfrac{\text{Wealth}_0(1+r_\text{nominal})^2}{\text{ApplePrice}_0(1+r_\text{inflation})^2} \\ &= \dfrac{100(1+0.0075)^2}{1(1+0.018)^2} \\ &= \dfrac{101.505625}{1.036324} \\ &= 97.9477702 \text{ apples or dollars}\\ \end{aligned}###The below table shows all missing values:

| Wealth in Dollars and Apples | ||||

| Time (year) | Bank account wealth ($) | Apple price ($) | Wealth in apples | |

| 0 | 100 | 1 | 100 | |

| 1 | 100.75 | 1.018 | 98.96856582 | |

| 2 | 101.505625 | 1.036324 | 97.9477702 | |

Commentary

Note that the negative real interest rate in early 2020 is unusual. When the economy is growing well and inflation is high within the RBA's 2 to 3% pa target band, real rates are usually positive to entice investors to save (lend or buy debt) rather than borrow (sell debt). However, in early 2020, the Australian central bank was afraid of a recession so they kept the overnight money market rate very low at 0.75% pa to encourage consumers to borrow and spend rather than save. The central bank is implementing expansionary monetary policy by keeping the interest rate so low since it encourages higher consumption and higher economic growth.

Question 353 income and capital returns, inflation, real and nominal returns and cash flows, real estate

A residential investment property has an expected nominal total return of 6% pa and nominal capital return of 3% pa.

Inflation is expected to be 2% pa. All rates are given as effective annual rates.

What are the property's expected real total, capital and income returns? The answer choices below are given in the same order.

The nominal total return and capital return are given, therefore the nominal income return can be calculated.

###r_\text{nominal, total} = r_\text{nominal, income} + r_\text{nominal, capital} ### ###0.06 = r_\text{nominal, income} + 0.03 ### ###\begin{aligned} r_\text{nominal, income} &= 0.06 - 0.03\\ &= 0.03 \\ \end{aligned}###The Fisher equation can be used to convert nominal rates to real rates. The exact version is:

###1+r_\text{real} = \dfrac{1+r_\text{nominal}}{1+r_\text{inflation}}###The approximation is:

###r_\text{real} \approx r_\text{nominal} - r_\text{inflation}###But the Fisher equation only applies to the total and capital returns, not the income return. This is obvious when considering the approximation of the Fisher equation. If inflation is subtracted from both the nominal capital and income returns, then since the total return is the sum of these two, inflation will be subtracted twice from the total return which is wrong.

Method 1: Fisher equation on total and capital returns

Work out the total and capital returns using the Fisher equation, then calculate the difference which is the income return.

To find the real total return:

###1+r_\text{real, total} = \dfrac{1+r_\text{nominal, total}}{1+r_\text{inflation}}### ###1+r_\text{real, total} = \dfrac{1+0.06}{1+0.02}### ###r_\text{real, total} = \dfrac{1+0.06}{1+0.02}-1 = 0.039215686 ###To find the real capital return:

###1+r_\text{real, capital} = \dfrac{1+r_\text{nominal, capital}}{1+r_\text{inflation}}### ###1+r_\text{real, capital} = \dfrac{1+0.03}{1+0.02}### ###r_\text{real, capital} = \dfrac{1+0.03}{1+0.02}-1 = 0.009803922 ###To find the real income return:

###r_\text{real, total} = r_\text{real, income} + r_\text{real, capital} ### ###0.039215686 = r_\text{real, income} + 0.009803922 ### ###\begin{aligned} r_\text{real, income} &= 0.039215686 - 0.009803922 \\ &= 0.029411765 \\ \end{aligned}###Method 2: Convert nominal cash flows to real cash flows

Discount all future nominal cash flows by inflation to get the real cash flows then calculate the real rates of return.

###\begin{aligned} r_\text{nominal, total} &= r_\text{nominal, income} + r_\text{nominal, capital} \\ &= \dfrac{C_\text{1, nominal}}{P_0} + \dfrac{P_\text{1, nominal}-P_0}{P_0} \\ \end{aligned}\\ \begin{aligned} r_\text{real, total} &= r_\text{real, income} + r_\text{real, capital} \\ &= \dfrac{C_\text{1, real}}{P_0} + \dfrac{P_\text{1, real}-P_0}{P_0} \\ &= \dfrac{ \left( \dfrac{C_\text{1, nominal}}{(1+r_\text{inflation})^1} \right) }{P_0} + \dfrac{\left( \dfrac{P_\text{1, nominal}}{(1+r_\text{inflation})^1} \right)-P_0}{P_0} \\ \end{aligned}\\###If the price now were, say, $1 then the nominal income cash flow in one period would be $0.03 which is the nominal income return times the price now. The nominal price in one period would be $1.03 ##(=1(1+0.03)^1)## which is the price now grown by the nominal capital return. Note that the price now ##(P_0)## is not affected by inflation. Substituting these and inflation into the above equation, the real returns can be calculated:

###\begin{aligned} r_\text{real, total} &= \dfrac{ \left( \dfrac{0.03}{(1+0.02)^1} \right) }{1} + \dfrac{\left( \dfrac{1.03}{(1+0.02)^1} \right)-1}{1} \\ &= 0.029411765 + 0.009803922 \\ &= 0.039215686 \\ \end{aligned}###So the real total return is 3.92%, the real capital return is 0.98% and the real income return is 2.94%.

Question 407 income and capital returns, inflation, real and nominal returns and cash flows

A stock has a real expected total return of 7% pa and a real expected capital return of 2% pa.

Inflation is expected to be 2% pa. All rates are given as effective annual rates.

What is the nominal expected total return, capital return and dividend yield? The answers below are given in the same order.

The Fisher equation can be used to calculate nominal and real rates. The exact version is:

###1+r_\text{real} = \dfrac{1+r_\text{nominal}}{1+r_\text{inflation}}###The approximation is:

###r_\text{real} \approx r_\text{nominal} - r_\text{inflation}###The only problem is that the Fisher equation only applies to the total and capital returns, not the income return. This is obvious when considering the approximation of the Fisher equation. If inflation is added to the real capital and income returns, then since the real total return is the sum of these two, inflation will be added twice to the total return which is wrong.

Method 1: Fisher equation on total and capital returns

Work out the total and capital returns using the Fisher equation, then calculate the difference which is the income return.

To find the nominal total return:

###1+r_\text{real, total} = \dfrac{1+r_\text{nominal, total}}{1+r_\text{inflation}}### ###1+0.07 = \dfrac{1+r_\text{nominal, total}}{1+0.02} ### ###r_\text{nominal, total} = (1+0.07)(1+0.02)-1 = 0.0914 ###To find the nominal capital return:

###1+r_\text{real, capital} = \dfrac{1+r_\text{nominal, capital}}{1+r_\text{inflation}}### ###1+0.02 = \dfrac{1+r_\text{nominal, capital}}{1+0.02} ### ###r_\text{nominal, capital} = (1+0.02)(1+0.02)-1 = 0.0404 ###To find the real income return:

###\begin{aligned} r_\text{nominal, total} &= r_\text{nominal, income} + r_\text{nominal, capital} \\ 0.0914 &= r_\text{nominal, income} + 0.0404 \\ \end{aligned}### ###\begin{aligned} r_\text{nominal, income} &= 0.0914 - 0.0404 \\ &= 0.051 \\ \end{aligned}###Method 2: Convert nominal cash flows to real cash flows

Grow all future real cash flows by inflation to get the nominal cash flows then calculate the nominal rates of return.

###\begin{aligned} r_\text{nominal, total} &= r_\text{nominal, income} + r_\text{nominal, capital} \\ &= \dfrac{C_\text{1, nominal}}{P_0} + \dfrac{P_\text{1, nominal}-P_0}{P_0} \\ &= \dfrac{C_\text{1, real}.(1+r_\text{inflation})^1}{P_0} + \dfrac{P_\text{1, real}.(1+r_\text{inflation})^1-P_0}{P_0} \\ \end{aligned}###If the price now were, say, $1 then the nominal income cash flow in one period would be $0.05 which is the nominal income return times the price now. The nominal price in one period would be $1.02 ##(=1(1+0.02)^1)## which is the price now grown by the nominal capital return. Note that the price now ##(P_0)## is not affected by inflation. Substituting these and inflation into the above equation, the real returns can be calculated:

###\begin{aligned} r_\text{nominal, total} &= \dfrac{C_\text{1, real}.(1+r_\text{inflation})^1}{P_0} + \dfrac{P_\text{1, real}.(1+r_\text{inflation})^1-P_0}{P_0} \\ &= \dfrac{0.05 \times (1+0.02)^1}{1} + \dfrac{1.02 \times (1+0.02)^1-1}{1} \\ &= 0.051 + 0.0404 \\ &= 0.0914 \\ \end{aligned}###So the real total return is 9.14%, the real capital return is 4.04% and the real income return is 5.1%.

Question 525 income and capital returns, real and nominal returns and cash flows, inflation

Which of the following statements about cash in the form of notes and coins is NOT correct? Assume that inflation is positive.

Notes and coins:

Notes and coins pay no income and therefore have zero nominal and real income returns. Since $100 of notes and coins are worth $100 now and will still be worth $100 in one year, the nominal capital return is zero. The nominal total return is the sum of the nominal income and capital return therefore it's also zero.

However, $100 of notes and coins will buy less goods and services in one year than it will now if inflation is positive because the price of things will increase. Therefore the real capital return and real total returns of notes and coins are negative.

Question 295 inflation, real and nominal returns and cash flows, NPV

When valuing assets using discounted cash flow (net present value) methods, it is important to consider inflation. To properly deal with inflation:

(I) Discount nominal cash flows by nominal discount rates.

(II) Discount nominal cash flows by real discount rates.

(III) Discount real cash flows by nominal discount rates.

(IV) Discount real cash flows by real discount rates.

Which of the above statements is or are correct?

Nominal cash flows can be discounted using nominal discount rates. Also, real cash flows can be discounted using real discount rates. Both will give the same asset price.

###C_\text{0} = \dfrac{C_\text{t, nominal}}{(1+r_\text{nominal})^t} = \dfrac{C_\text{t, real}}{(1+r_\text{real})^t}###If the cash flows are nominal and the discount rate is real or vice-versa, it's usually easier to convert the discount rate to a nominal or real rate using the Fisher equation, and then discount the cash flows to arrive at the correct price.

###1+r_\text{real} = \dfrac{1+r_\text{nominal}}{1+r_\text{inflation}}###Cash flows can also be converted from nominal to real or vice versa using the inflation rate.

###C_\text{t, real} = \dfrac{C_\text{t, nominal}}{(1+r_\text{inflation})^t}###Question 526 real and nominal returns and cash flows, inflation, no explanation

How can a nominal cash flow be precisely converted into a real cash flow?

No explanation provided.

Question 575 inflation, real and nominal returns and cash flows

You expect a nominal payment of $100 in 5 years. The real discount rate is 10% pa and the inflation rate is 3% pa. Which of the following statements is NOT correct?

If all goods and services' nominal prices grow by the same inflation rate, then their real prices will be unchanged or constant.

For example, say apples and oranges originally cost $1 each, so one apple is worth one orange. Then a year later, they cost $1.03 each since inflation was 3% pa. Since one apple is still worth one orange, the real price of apples and oranges is the same. It's only the nominal price (in dollars) that has changed.

Therefore only nominal prices increase by inflation. Real prices are unaffected.

Question 577 inflation, real and nominal returns and cash flows

What is the present value of a real payment of $500 in 2 years? The nominal discount rate is 7% pa and the inflation rate is 4% pa.

The real cash flow cannot be discounted by a nominal discount rate.

Method 1: Discount the real cash flow by the real discount rate

The nominal discount rate can be converted into a real rate using the Fisher equation.

###1+r_\text{real} = \dfrac{1+r_\text{nominal}}{1+r_\text{inflation}}### ###1+r_\text{real} = \dfrac{1+0.07}{1+0.04}### ###\begin{aligned} r_\text{real} &= \dfrac{1+0.07}{1+0.04} -1 \\ &= 0.028846154 \\ \end{aligned}###Now discount the real payment by the real discount rate.

###\begin{aligned} V_0 &= \dfrac{V_\text{2, real}}{(1+r_\text{real})^2} \\ &= \dfrac{500}{(1+0.028846154)^2} \\ &= 472.3556643 \\ \end{aligned}###Method 2: Discount the nominal cash flow by the nominal discount rate

The real cash flow can be converted into a nominal cash flow by growing using the inflation rate:

###V_\text{2, real} = \dfrac{V_\text{2, nominal}}{(1+r_\mathbf{inflation})^2} ### ###500 = \dfrac{V_\text{2, nominal}}{(1+0.04)^2} ### ###\begin{aligned} V_\text{2, nominal} &= 500 \times (1+0.04)^2 \\ &= 540.8 \\ \end{aligned}###Now discount the nominal payment by the nominal discount rate.

###\begin{aligned} V_0 &= \dfrac{V_\text{2, nominal}}{(1+r_\text{nominal})^2} \\ &= \dfrac{540.8 }{(1+0.07)^2} \\ &= 472.3556643 \\ \end{aligned}###Question 554 inflation, real and nominal returns and cash flows

On his 20th birthday, a man makes a resolution. He will put $30 cash under his bed at the end of every month starting from today. His birthday today is the first day of the month. So the first addition to his cash stash will be in one month. He will write in his will that when he dies the cash under the bed should be given to charity.

If the man lives for another 60 years, how much money will be under his bed if he dies just after making his last (720th) addition?

Also, what will be the real value of that cash in today's prices if inflation is expected to 2.5% pa? Assume that the inflation rate is an effective annual rate and is not expected to change.

The answers are given in the same order, the amount of money under his bed in 60 years, and the real value of that money in today's prices.

The nominal amount of money that he will have in 60 years is simply the sum of the monthly payments since money under the bed doesn't pay any interest!

###\begin{aligned} V_\text{60yrs, nominal} &= 60 \times 12 \times 30 \\ &= 21,600 \\ \end{aligned}###The real value in today's prices of the money that will be under his bed in 60 years is also the sum of the monthly payments, but it's discounted by the inflation rate over the 60 years.

###\begin{aligned} V_\text{60yrs, real} &= \dfrac{60 \times 12 \times 30}{(1+r_\text{inflation pa})^{60}} \\ &= \dfrac{21,600}{(1+0.025)^{60}} \\ &= 4909.325498 \\ \end{aligned}###Question 745 real and nominal returns and cash flows, inflation, income and capital returns

If the nominal gold price is expected to increase at the same rate as inflation which is 3% pa, which of the following statements is NOT correct?

The real income return of gold is zero since it pays nothing. No interest, dividends or rent. The nominal income yield on gold is also zero. Income yields are generally not affected much by inflation, unlike capital returns and total returns. One way to calculate the real income return from the nominal income return is:

###\begin{aligned} r_\text{real income} &= \dfrac{C_\text{1,real}}{P_0} \\ &= \dfrac{C_\text{1,nominal}/(1+r_\text{inflation})^1}{P_0} \\ &= \dfrac{\left(\dfrac{C_\text{1,nominal}}{P_0}\right)}{(1+r_\text{inflation})^1} \\ &= \dfrac{r_\text{nominal income}}{1+r_\text{inflation}} \\ &= \dfrac{0}{1+0.03} \\ &= 0 \\ \end{aligned}###Question 732 real and nominal returns and cash flows, inflation, income and capital returns

An investor bought a bond for $100 (at t=0) and one year later it paid its annual coupon of $1 (at t=1). Just after the coupon was paid, the bond price was $100.50 (at t=1). Inflation over the past year (from t=0 to t=1) was 3% pa, given as an effective annual rate.

Which of the following statements is NOT correct? The bond investment produced a:

All statements are true except for (e). This is because the current stock price of $100 should not be discounted by the inflation rate since it is a value now that is both real and nominal, there's no need to convert it to real. Only the nominal stock price in one year of $100.50 should be discounted by the inflation rate to convert it into a real value in one year.

###\begin{aligned} P_\text{T real} &= P_\text{T nominal}/(1+r_\text{inflation})^T \\ \end{aligned}### ###\begin{aligned} r_\text{real capital} &= \dfrac{P_\text{1 real} - P_0}{P_0} \\ &= \dfrac{P_\text{1 nominal}/(1+r_\text{inflation})^1 - P_0}{P_0} \\ &= \dfrac{100.5/(1+0.03)^1 - 100}{100} \\ &= -0.024271845 \\ \end{aligned}###An alternative method to find the real capital return is to use the exact Fisher equation which gives the same solution.

You're considering making an investment in a particular company. They have preference shares, ordinary shares, senior debt and junior debt.

Which is the safest investment? Which has the highest expected returns?

If a firm goes bankrupt, investors in different securities get paid back in this order:

- Senior debt

- Mezzanine debt

- Junior debt

- Preferred shares

- Ordinary shares

Ordinary stock holders get paid back last and only if there are any assets remaining, so they have the highest risk and deserve the highest return.

Senior debt gets paid first so it has the lowest risk and deserves the lowest yields (returns are usually called yields for debt).

Which business structure or structures have the advantage of limited liability for equity investors?

Corporations have the advantage of limited liability, so equity investors will never lose more than the amount that they have invested in the company. On the other hand, sole traders and partners can be sued and forced to sell their personal assets such as their house and property if the business's assets are insufficient to cover its liabilities.

Therefore sole traders', partners' and corporate shareholders' business equity are at risk. But sole traders' and partners' personal assets are also at risk whereas corporate shareholders' personal assets are safe due to limited liability.

Question 531 bankruptcy or insolvency, capital structure, risk, limited liability

Who is most in danger of being personally bankrupt? Assume that all of their businesses' assets are highly liquid and can therefore be sold immediately.

Darren has negative equity in his business. His business equity is -$7,000 since the business's liabilities of $10,000 are greater than its assets of $3,000. Since the business is a sole tradership rather than a company, Darren is personally liable for the business's debts.

Darren's non-business personal assets of $10,000 less personal liabilities of $6,000 net to $4,000. Therefore Darren's total personal wealth including the business is -$3,000 (=4,000-7,000), so he is most in danger of going bankrupt when the business's liabilities have to be repaid.

Notice that Billy's business also has negative equity of -7,000 (=3,000-10,000) and therefore his company is in danger of going bankrupt when its debts are due. However, since the business is a company, Billy will not be personally liable for those debts. He won't have to pay them, unlike Darren whose business is not a company.

Which of the following statements about book and market equity is NOT correct?

The statement in answer C is untrue. A company's book value of equity is recorded in its balance sheet, also known as the statement of financial position.

The below screenshot of Commonwealth Bank of Australia's (CBA) details were taken from the Google Finance website on 7 Nov 2014. Some information has been deliberately blanked out.

What was CBA's market capitalisation of equity?

The market capitalisation of equity ##(E)## equals the number of shares ##(n)## multiplied by the market share price ##(p)##.

###\begin{aligned} E &= n.p \\ &= 1.62b \times 82.76 \\ &= 134.07b \\ \end{aligned}###Question 444 investment decision, corporate financial decision theory

The investment decision primarily affects which part of a business?

The investment decision is about what assets the business should buy. Managers are supposed to buy assets that increase shareholder wealth. Buying undervalued assets is the best way to do this. The business project of buying the undervalued asset and then selling it for a higher price or using it to generate cash flow would be called a positive net present value (NPV) project.

Question 445 financing decision, corporate financial decision theory

The financing decision primarily affects which part of a business?

The financing decision is about how to finance the business's assets. If there isn't enough cash to buy assets, more cash must be raised by issuing liabilities such as loans, bills or bonds or by issuing shares.

Question 443 corporate financial decision theory, investment decision, financing decision, working capital decision, payout policy

Business people make lots of important decisions. Which of the following is the most important long term decision?

The investment decision determines what assets to buy to carry on the business. If managers buy assets that fail to create enough revenue to cover costs then the business will eventually fail.

The expression 'you have to spend money to make money' relates to which business decision?

The saying 'you have to spend money to make money' alludes to the idea that you have to buy assets to generate income, which relates to the investment decision. Perhaps the saying would be better phrased as 'you have to invest money (in assets) to make money (generate income and capital gains)'.